Since the beginning of the last century, some of the most progressive visionaries have boldly stated that for the continent to achieve sustainable economic growth, African nations must carve a path to prosperity without foreign dependence.

Yet, the continent’s challenges are still highly conspicuous, and the progress is painstakingly slow.

Some of the most significant issues the continent faces include unemployment and underemployment. By 2019, the unemployment rate in sub-Saharan Africa stood at around 6%, according to the International Labour Organization. ILO further stated that the work available is unskilled or low-skilled, partly because Africa has the world’s lowest levels of access to higher education.

So, despite many people in the continent having jobs, 70% of sub-Saharan Africa’s workforce is vulnerable compared to the global average of 46%. It is, therefore, that business leaders are focusing on solving unemployment and underemployment issues in Africa.

Far from unemployment, Africa faces other issues such as underinvestment in infrastructure, fiscal policies, climate change, and political changes disrupting business policies across the continent. But the biggest problem that most experts often cite as an impediment to economic growth is Africa’s dependence on commodities.

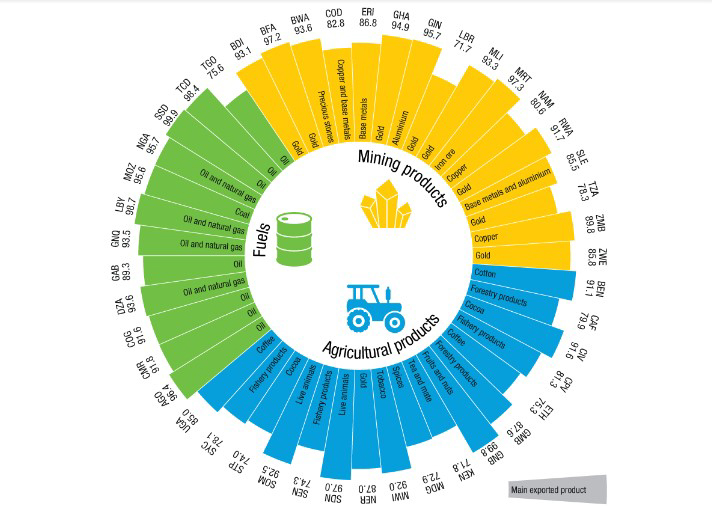

According to a 2022 UNCTAD report, commodities account for over 60% of total merchandise exports in 45 of the 54 countries in Africa. This leaves the continent vulnerable to global commodity price shocks, further undermining Africa’s inclusive growth and development potential.

Here is a chart showing how African countries depend on commodities according to UNCTAD. A country is considered dependent on a commodity when these products make up more than 60% of its total merchandise exports.

From the above figure, 83% of African countries are commodity-dependent, accounting for 45% of the commodity-dependent countries worldwide. One can also tell that the continent has some of the most invaluable assets that can power the world – natural resources.

The African continent holds an outsize proportion of natural resources globally. The UN’s Environment Programme says that Africa has approximately 30% of the world’s mineral reserves, fossil fuels reserves of about 8% of the world’s natural gas and 12% of its oil. It further states that Africa contains 65% of the global arable land and 10% of its internal renewable fresh water.

But despite the potential of these natural resources to power economic transformation, Africa still struggles to leverage its resource wealth to achieve practical change and development prospects.

The good news is that Africa can use its natural resources to position itself as a global economic powerhouse. The burgeoning youth population will largely provide the workforce needed to make this dream a reality. After all, the World Bank estimates that by 2050 half of the 1 billion people in sub-Saharan Africa will be under the age of 25. This stresses the need for creating employment opportunities for the continent’s youth.

Using its natural resources and the increasing workforce, Africa can shift from export-focused economies to a more diversified set that includes information and value-added manufacturing economies. But resources and sheer numbers alone are insufficient to create this change for the continent.

Both will require the right partnerships, management, and investment to serve as the backbone of a global economy. Enter Equity Group.

Recognizing the need to ship from dependence on exports to making Africa self-reliant, Equity Group launched the Africa Resilience plan, a 678-billion-shilling private sector-focused package to accelerate African economic growth.

The plan puts women, the youth, and Africa’s natural resources at the heart of Africa’s economic and social development. Some of the solutions Equity is committed to achieving include:

Building Local and National Economies Through Social Support

Equity takes a local-first approach to building local and national economies. This involves making cities and villages more productive and sustainable. This is predicated on offering social assistance and capacity building to poor, vulnerable, and marginalized populations and transitioning beneficiaries from systemic dependence on aid to self-reliance.

Some of the interventions in this stage include safety net programs, financial literacy training for refugees and vulnerable households, and support for easy access to digital inclusion tools.

Equity’s local first approach provides incentives for investments in small and medium-sized enterprises, skilling communities, and helping entrepreneurs focus on high-growth industries. Precedence will be put on the vulnerable, such as the youth and women.

So far, under social support, Equity has reached 4 million households and disbursed 100.7 billion shillings through its 22 successfully operating programs in Kenya, Rwanda, Uganda, and South Sudan.

Preparing Youth for High-Growth Industries

In addition to upskilling the youth at the community level, Equity Group has invested heavily in supporting young talent in Kenya. The bank has, so far, offered 37,009 secondary school scholarships and supported 17,040 scholars in universities, 3,262 students in TVET institutions, and 715 students in global universities.

This commitment springs from fully realising that sustainable local economies and stable labour forces are built upon a strong foundation of education and skilling. Its support in the education sector and through the Equity Leadership Program will go a long way in reducing the over 60% of youth ages 15-17 in sub-Saharan Africa who are not in school. This is the population that’s primed to begin entering the workforce.

Creating Job Opportunities for Women and Youth

Experts from the Africa Growth Initiative proffer that every year, there will be 8-9 million new entrants into the African labour force. A multi-faceted approach across all businesses in Africa and sectors is required to provide good jobs for these entrants.

One of the ways of doing this is by encouraging the growth of youth startups, which often play a significant role in economic transformation and employment creation by using newer technology.

But since SMEs employ most people in Africa, building a healthy culture of entrepreneurship across these small businesses will come in handy. To this end, Equity Group plans to lend and advance loans to 5 million MSMEs and 25 million individuals to stimulate the local community and population’s participation, specifically focusing on young people and women.

Strong support for MSMEs would enhance Equity Group’s overall aim to generate 25 million new direct employment as businesses expand and an additional 25 million indirect jobs as value chains deepen and widen. This is consistent with Sub-Sahara’s requirement to generate millions of jobs in the upcoming years to accommodate the region’s growing population.

Modernize and Develop Sustainable ‘Green’ Industries

Technology is driving innovation and growth worldwide across various industries. This presents an excellent opportunity for Africa to grow, particularly if partnered with a rapidly growing, working-age, skilled, and educated youth population.

Agriculture, for example, constitutes up to 60% of the total employment in sub-Saharan Africa. This food system will create more jobs between 2010 – 2025 than all the other industries combined. Yet, technology remains underutilized in the sector.

The sound development of tech will go a long way in creating efficiencies and scale in all sectors, including agriculture, mining, infrastructure projects, forestry, extraction industries, and construction. And this will serve as the vanguard for vibrant economies.

Better still, African nations should support the growth of industries based on the massive trove of renewable energy such as solar and wind. The continent can use technology to transition its industries from fossil fuel dependence to renewable sources and energy production.

Luckily, Equity Group’s mandate to reduce the carbon footprint in the country has made various strides through conservation and promoting the use of renewable energy. Its interventions, which include transitioning industries and households to clean energy, increasing the adoption of low-carbon production technology, and investments in climate-smart technologies, are paying off.

Equity has reached 339,146 households with renewable energy products impacting over 1.35 million individuals, with households realizing over 3.78 billion shillings by switching to clean energy and reducing 360,000 metric tons of carbon dioxide.

Apart from these interventions, Equity has other focus pillars and robust strategies for each – geared toward making Africa self-reliant economically. Of course, the vision is viable, but it also requires the African nations’ political will and their partners’ support.

Read more about the Africa Resilience Plan through this link.

Equity Bank Balance Sheet to Hit Ksh 3 Trillion Mark by 2025