Outsized external inflows from international financial institutions and commercial financing are expected in the coming month. This flash note assesses the lumpy inflows against the FY20/21 budget outturn.

We estimate an aggregate KES 264.1Bn from both multilateral and commercial financing (Eurobond IV). (Figure 1) that is expected in the final month of this fiscal year (June 2021). Undoubtedly, these flows will support KES stability in the near term. As per our 10M20/21 Fiscal performance topical note, we noted external financing in April increased by KES 46.7Bn, which comprised of KES 33.7Bn initial IMF disbursement for its ongoing 38-month program with the remainder (KES 13.0Bn) being the funding of development projects (project cash loans and project loans Appropriation-in-Aid, AiA).

Figure 1: External financing from multilateral institutions and commercial financing

Source: 2021 Budget Policy Statement *Extended Fund Facility and Extended Credit Facility **third Development Policy Operation

As of the end of the ten months in this fiscal year (10M20/21), the National Treasury reported net foreign financing at KES 112.50Bn, which translates to KES 306.30Bn disbursements in the months of May and June. As per Figure 1, we can account for KES 264.1Bn, which means that the remainder is project funds. Nonetheless, the absorption of development funds has been sluggish, trailing its target by KES 59.4Bn (-37.3%) at the end of 9M20/21. For argument’s sake, we assume that this balance (c. KES 42.2Bn) is disbursed in its entirety in these final two months of the fiscal year.

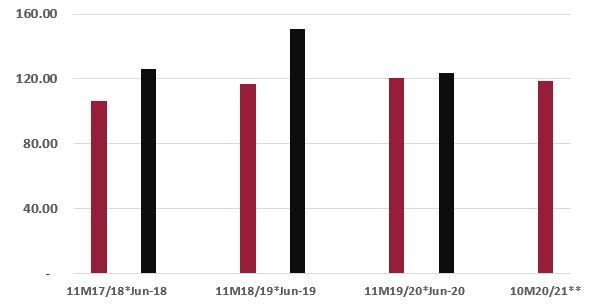

In addition to this expected lumpy external financing, we do not discount the anticipated outsized tax receipts in June. As Figure 2 indicates, the subject month has historically recorded elevated tax receipts in comparison to the average in the hitherto 11 months. For the current fiscal year, we calculate a monthly average of KES 119.1Bn in the first 10 months of FY20/21 and estimate June tax receipts at KES 138.9Bn.

Figure 2: Tax receipts, KES, Bn’s

Source: National Treasury, Genghis Capital *monthly average in the first 11 months of that fiscal year

**monthly average in the first 10 months of this fiscal year

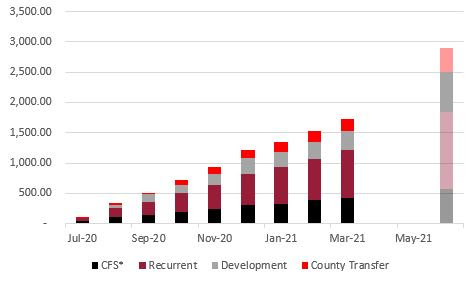

This takes us to the next critical issue. At a fundamental level, the question that keeps popping in our heads is how fast the outsized flows (external financing and tax receipts) will be deployed. Specifically, Figure 3 is indicative of budget expenditure (excluding debt redemptions) outturn in the first 9 months of the fiscal year. Notably, KES 1.73Tn was the aggregate budget spending (excluding debt redemptions) in the period. This implies that KES 1.16Tn remains pending at the start of this final quarter (FY20/21 target: KES 2.89Tn).

Figure 3: Budget Expenditure in FY20/21, KES, Bn’s

Source: National Treasury, Genghis Capital *Consolidated Fund Services, net of debt redemptions NB: June 2021 level is the target following FY2020/21 Supplementary I

This notwithstanding, we flagged the low absorption of funds as of the end of April 2021. To be exact, net disbursements for recurrent and development hit KES 826.0Bn and KES 258.2Bn, respectively.

These figures represented a performance rate of 76.2% and 64.3%, respectively, of the overall FY20/21 targets. Disbursements to counties hit KES 239.8Bn, representing 62.5% of the overall fiscal year’s target.

As the leopard doesn’t change his spots, we are less convinced that the outsized flows will make up for the lost ground of budgetary execution. Figure 4 cements our view. In the period FY14/15 – FY19/20, the budget spending outturn has been an average of 90.4%. This goes counter to the ambitious budget spending targets that have played out in each fiscal year. We know that everyone needs a dose of motivation once in a while, but to literally apply, ‘Aim above the mark, to hit the mark’, in matters fiscal is a tad reckless. Plus it erodes the credibility of budget implementation. We thus opine that even as the FY21/22 budget is firmed up, recent budget outturns support the case for a pivot away from a KES 3.6Tn budget and to a more realistic lower level.

Figure 4: Budget Outturn, KES, Bn’s

Source: National Treasury, Genghis Capital

Source: National Treasury, Genghis Capital

One final thing as we roll into the final month of the fiscal year. That domestic borrowing is ahead of the curve, before rolling into the final month this FY20/21, is well telegraphed in the market.

T-Bills have reversed the uptrend that they have pencilled since July 2020. Month-to-date, yields on the 182-day and 364-day is down 12bps (0.12%) and 32bps (0.32%), respectively.

Market action this week has picked up the cue with elevated trading in the infrastructure bond segment (c. 53% of the Monday-to-Thursday trades). The domestic borrowing trajectory has teed up the odds of a longer tenor primary bond issuance in June. Against the backdrop of elevated external financing flows and moonshot tax receipts next month, we think infrastructure bond trading will continue dominating. We like IFB1/2021/18 at 12.10% – 12.15% levels.

Genghis Research is an innovative and customer-focused investment solutions provider licensed by the Capital Markets Authority (CMA) and the Retirement Benefits Authority (RBA). The company started off as a stock brokerage firm in 2008.