The coronavirus outbreak is providing an opportunity for Kenyan citizens to move to digital.

The Central Bank of Kenya on Monday met with Payment Service Providers (PSPs), to announce a set of measures that will facilitate increased use of mobile money transactions instead of cash.

“While the immediate objective is to reduce the risk of transmission of COVID-19 (Coronavirus) by handling banknotes, this will also reduce the use of cash in the economy over the medium term,” said the CBK in a statement.

Kenya enjoys a robust ICT sector. In its Global Innovation Index (GII) 2019 survey, Kenya was ranked the second-leading innovation center in sub-Saharan Africa by the World Intellectual Property Organization.

The number of mobile subscriptions (SIM1 Cards) in the country stood at 53.2 million as at 30th September 201933 which is a translation level of 112.0 percent to mobile (SIM) penetration.

“This upward trajectory of mobile penetration can be attributed to the availability of mobile signals and diverse traditional mobile services. The population covered by 2G and 3G is 96 percent and 93 percent respectively,” according to Communications Authority of Kenya, First Quarter Sector Statistics Report for the Financial Year 2019/2020 (July – September 2019).

Further, the report acknowledges Kenya as one of the world’s leading proponents of financial inclusion that has seen the proliferation of digital finance and payment platforms such as M-Pesa, Mula, PesaLink and Pesapal gain wide usage in the country.

“The increased adoption of these technologies continues to facilitate transactions and therefore enhance trade for individuals and small and medium-sized enterprises (SMEs),” says Kenya ICT Action Network (KICTANet) in its report Assessing Internet Development In Kenya: Using Unesco Internet Universality Roam-x Indicators.

https://khusoko.com/2020/03/16/safaricom-waives-fees-for-m-pesa-transfers-free-for-ksh1000/

CA estimates that the number of active mobile money subscribers, and agents by the end of 2019 stood at 31.2 million, and 235.168 respectively.

Towards the end of 2019, 425.3 million mobile trading transactions valued at Kenya shillings 1.6 trillion were spent on online purchases of goods and services.

“Overall, given the considerable actions taken by the government in the ICT sector over the last four to five years, which are starting to bear fruit, there is still great opportunity to address some issues including ICT skills, access (to devices and services), costs (of devices and services) and generally nurture increased usage among both businesses and residents,” KICTANet observed in its draft report.

The Kenya Bankers Association (KBA) in collaboration with the Customer Service Working Group Customer Satisfaction report released in February found out that, bank clients rated their satisfaction level at 83 percent based on banks’ responsiveness and service quality.

Out of more than 11,000 respondents surveyed, 32 percent indicated their digital experience was ‘’Exceptional’’ with 42 percent scoring banks’ digital services as ‘’Very Good’’.

Citing mobile banking (34 percent) and the efficiency of digital platforms (19 percent), 20 percent of respondents said their experience was ‘Good’ as 4.9 percent underlined their experience as ‘’Fair’’ and ‘’Unsatisfactory’’ (0.9 percent).

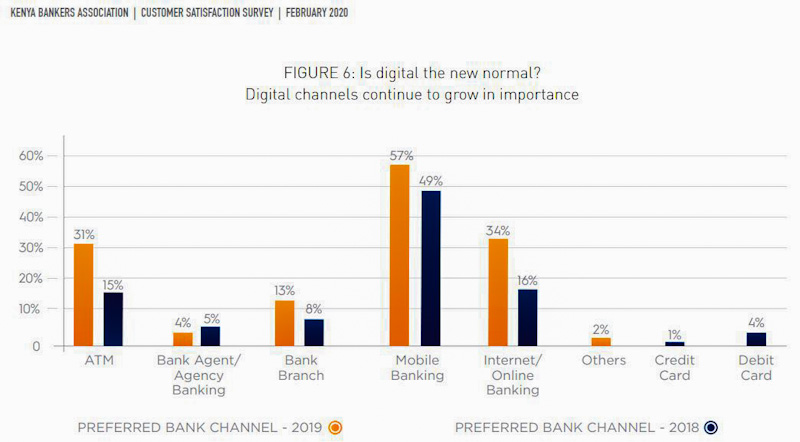

In the findings, the use of mobile banking rose to 57 percent in 2019 from 49 percent recorded in 2018. The spike was also experienced in the utilization of Internet banking channels, whose preference doubled from 16 percent in 2018 to 34 percent the following year.

These transformations have been enabled by banks’ continued investment in lower-cost digital capabilities which have consequently boosted customers’ adoption given their simplicity and convenience,’ the survey reports, adding that fully-automated banking services were preferred more in 2019 (24 percent) compared to 2018( 5 percent).

“The increase in use of technology by banks has been driven mainly by stiff competition among the banks. The banks have had to adopt cost-effective delivery channels in offering financial services to ensure efficiency and maintain their market shares,” CBK said in its report in the year to December 2019.

The CBK data showed Kenyans moved KSh4.35 trillion through their mobile phones last year, a 9.3 percent jump from2018. This was 3.7 times more than the KSh1.17 trillion that was transacted in 2011.

Alternative banking channels

Mobile banking: services offered may include facilities to conduct bank and stock market transactions, administer accounts and to access customized information.

Mobile networks in Kenya offer mobile money services in the name of M-PESA by Safaricom, Orange Money by Orange, and Airtel Money by Airtel.

Agent Banking: According to the Central Bank of Kenya’s guidelines on agent banking, agency banking is then the provision of banking services by a third – party agency to customers on behalf of a licensed, prudentially – regulated financial institution, such as a bank or any other deposit-taking commercial bank.

Agency banking was made legal following an amendment to the Banking Act 2010.

A bank agent is usually equipped with an EMV certified P.O.S. terminal with which they can process withdrawals and deposits after the consumer swipes their EMV certified bank debit or credit card.

These P.O.S. devices connect to the core banking system via a GPRS data connection using any of the major MNOs’ networks. Examples of banks that have Agent banking include Equity Group, Co-operative Bank, Family Bank Kenya, and Kenya Commercial Bank.

Internet Banking: This is a web-based service that allows you to transact online. It’s convenient, easy to use and allows you to do your banking securely via the Internet 24 hours a day, 7 days a week. One can pay for utilities, make bulk payments, transfer cash from one account to another.

Automated teller machine (ATM): This is an electronic banking outlet that allows customers to complete basic transactions without the aid of a branch representative or teller. Anyone with a credit card or debit card can access most ATMs.

Cards: Debit cards are also known as bank cards, check cards or plastic cards. A debit card can be used while making purchases and withdrawing cash at Automated Teller Machines (ATMs) or at an agent merchant point of sale (POS).

A credit card, on the other hand, allows the user to spend money that they currently do not possess in their account against a line of credit, which is the cards’ credit limit. The card’s credit limit is agreed upon when the credit card user enters into a contract with the bank in order to be issued with the card.