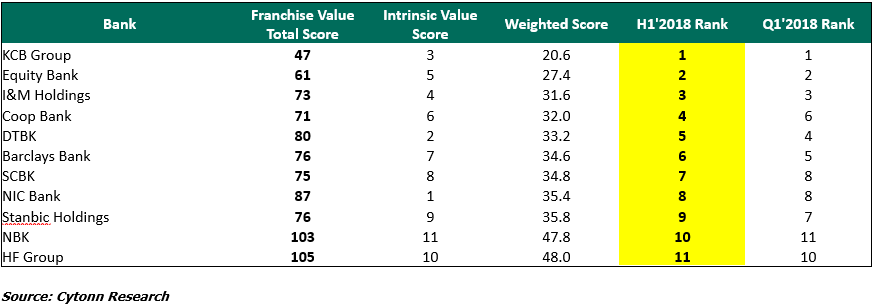

Kenya Commercial Bank (KCB) has been ranked as the most attractive bank in Kenya, a position it has retained since FY’2016, supported by a strong franchise value and intrinsic value score.

The franchise score measures the broad and comprehensive business strength of a bank across 13 different metrics, while the intrinsic score measures the investment return potential.

Cytonn Investments in their latest H1’2018 Banking Sector Report, KCB Group ranked first on the back of a high return on average equity of 21.9 percent, compared to an industry average of 19.5 percent, as well as high efficiency, with a Cost to Income Ratio of 52.0 percent, compared to an industry average of 55.7 percent.

Housing Finance Group ranked lowest overall, ranking last in the Franchise value score.

The report, themed ‘Growth and Efficiency aided by Technology, amid deteriorating Asset Quality’, analyzed the results of the listed banks using their H1’2018, unaudited results so as to determine which banks are the most attractive and stable for investment from a franchise value and from a future growth opportunity perspective,” said Ian Kagiri, Investment Analyst at Cytonn Investments.

“Banks will continue to put more emphasis on alternative revenue streams to boost their Non-Funded Income and adopt an efficient operating model through alternative banking channels and digitization in order to remain profitable under the tough operating environment of compressed margins”, added Ian.

“We have looked at four key focus areas, which are regulation, diversification, technology and asset quality in this report. With a tighter regulatory environment following the capping of interest rates and adoption of IFRS 9, diversification of revenue, cost management and asset quality management will prove to be the key growth drivers for players banking sector.”

In the report, Co-operative Bank rose 2 positions to position 4 from position 6 in Q1’2018, owing to its optimal loan to deposit ratio of 84.6 percent, above the industry average of 73.6 percent, a relatively high net interest margin of 8.6 percent, above the industry average of 8.1 percent, and the highest capitalization with a tangible common ratio of 16.8 percent, above the industry average of 14.4 percent.

Kenya’s listed banks recorded a 19.0 percent growth in core EPS growth in H1’2018, compared to a decline of 14.4 percent in H1’2017, and a 5-year average growth of 6.7 percent.

Only NIC Group and Housing Finance Group recorded declines in core EPS, registering declines of 2.1 percent and 95.7 percent, respectively.

Deposits grew at 10.0 percent y/y, a faster rate than loans, which grew by 3.8 percent.

The loan growth came in lower as private sector credit growth remained low at an average of 2.5 percent, in the 8 months to August 2018 below the five-year average of 13.0 percent, with banks adopting a more prudent credit risk assessment framework to ensure quality loan books so as to manage the rising non-performing loans.

KCB Retains its Spot as Most Attractive Bank for Investors

Khusoko

Khusoko provides market insights into Africa's business investment as well as global trends that impact East African businesses.