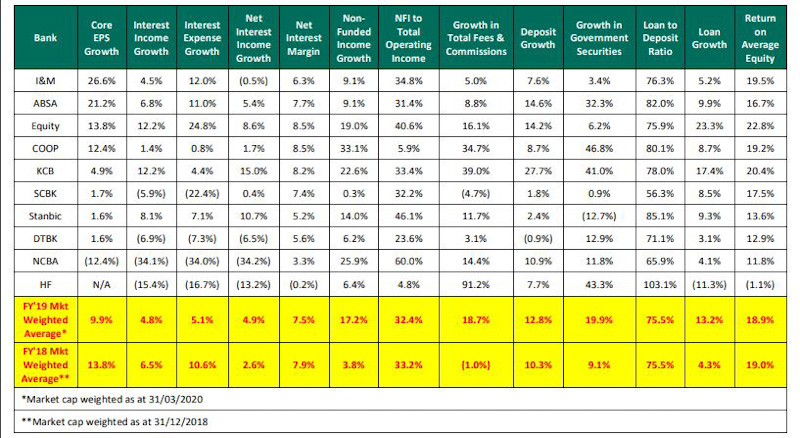

The Kenyan banking sector had strong growth in 2019 compared to the performance recorded in a similar period last year.

According to Cytonn Investments’ Kenya Listed Banking Sector Earnings Performance– FY’2019’ the banking sector grew by 4.9 percent in 2019 compared to a growth of 13.8% in FY’2018.

“The slower 4.8% growth in interest income compared to the 6.5% recorded in FY’2018, may be attributable to the lower yields on interest-earning assets compared to FY’2018. Consequently, the Net Interest Margin (NIM) in the banking sector currently stands at 7.5%, a decrease from the 7.9% recorded in FY’2018, despite the Net Interest Income increasing by 4.9% y/y.”

Kenya listed banks recorded a 9.9 per cent average increase in core Earnings Per Share, compared to a growth of 13.8% percent in 2018.

However, eight of the ten listed banks recorded growth in core earnings per share, save for NCBA and HF group, which slipped to core losses. I&M Holdings recorded the highest growth of 26.6%, and the lowest being HF Group, which recorded a loss per share of Kshs 0.3.

Deposit growth

The sector recorded strong deposit growth, which came in at 12.8%, faster than the 10.3% growth recorded in FY’2018. Despite the relatively fast deposit growth, interest expenses growth of 5.1% was slower than the 10.6% growth recorded in FY’2018, indicating that banks have been able to mobilize relatively cheaper deposits after the September 2018 implementation of the Finance Act 2018, which saw the removal of the minimum interest rate payable on deposits, which stood at 70.0% of the Central Bank Rate (CBR).

This helped mitigate high increments in interest expense, despite the relatively fast deposit growth.

Loan growth

Average loan growth came in at 13.2%, which was faster than the 4.3% recorded in FY’2018, indicating that there was an improvement in credit extension, with banks targeting select segments such as corporate entities and Small and Medium Enterprises (SMEs), the growth in loans was accelerated towards the tail end of FY’2019 following the repeal of interest rate cap in November 2019.

Government securities, on the other hand, recorded a growth of 19.9% y/y, which was faster compared to the loans and the 9.1% growth recorded in FY’2018. This highlights banks’ continued preference towards investing in government securities, which offer better risk-adjusted returns.

Interest income

Interest income increased by 4.8%, compared to a growth of 6.5% recorded in FY’2018. The slower 4.8% growth in interest income compared to the 6.5% recorded in FY’2018, may be attributable to the lower yields on interest-earning assets compared to FY’2018.

Consequently, the Net Interest Margin (NIM) in the banking sector currently stands at 7.5%, a decrease from the 7.9% recorded in FY’2018,

despite the Net Interest Income increasing by 4.9% y/y.

Non-funded Income

Non-funded Income grew by 17.2% y/y, faster than 3.8% recorded in FY’2018. The growth in NFI was supported by the 18.7% average increase in total fee and commission income, which was faster than the (1.0%) growth recorded in FY’2018.

Source: Cytonn Investments.