Safaricom on Friday reported its earnings before interest, taxation, depreciation, and amortization (EBITDA) in the full year to March soared 13.1% to Ksh89.6 billion.

This was driven by M-Pesa growing at 19.2% year on year, and, accounting for 75% of the revenue growth for the year.

• Service revenue growth of 7% to KSh 240.30bn.

• Voice service (incoming and outgoing) revenue grew by 0.3% to KSh95.94bn.

• M-PESA revenue grew by 19.2% to KSh 74.99bn.

• Mobile data revenue increased by 6.4% to KSh38.69bn.

• Fixed service revenue increased by 22.7% to KSh8.19bn.

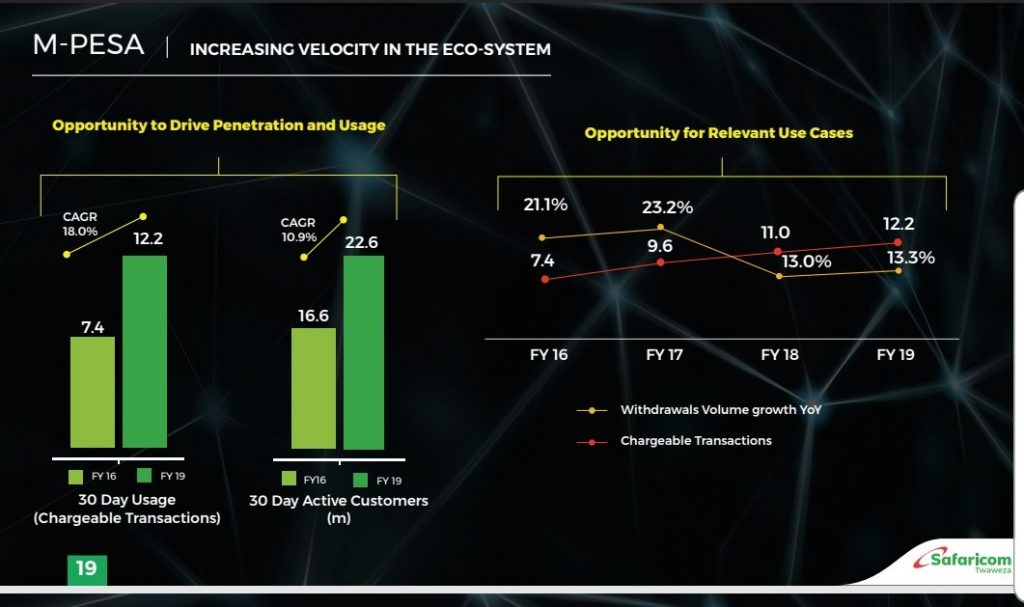

• Total customer base increased by 7.7% to 31.8m.

• 30-day active M-PESA customers increased by 10.2% to 22.6m.

• 30-day active mobile data customers increased by 6.6% to 18.8m.

Chief Executive Officer Safaricom Bob Collymore said the improvement in the company’s performance continues to reflect growth even in the months to come.

“We are pleased with the strong results we have for the year, building on our long track record of delivering relevant products and putting the customer first. We foresee continued growth in the future,” he said.

The earnings of mobile data from the listed telecommunication firm increased by 6.4% to Sh38.7 billion while the fixed service revenue grew by 22.7% to Sh8.9 billion.

The company’s Chief Executive Officer Bob Collymore said the company expects to register growth through the delivery of quality services to its customers.

“Looking ahead, the business will sustain its momentum of investing in the quality of our service and diversification of our revenue portfolio to ensure sustained returns to shareholders,” said Collymore.

M-Pesa to pass 50% mark in 3-4 Years

“We expect it to go past the 50% mark, probably in about three or four years but we are also looking at other revenue streams,” said Collymore citing efforts to boost revenue from digital services for farmers dubbed Digifarm.

The telco has proposed a Ksh 50 billion an increase of 13.6% (Ksh1.25 per share). It also proposed special dividends of Ksh 20 billion to its shareholders. The two are subject to approval from the shareholders when they hold the Annual General Meeting.

****

A 14.7% growth in bottom-line numbers in the current economic environment indicates a resilient business with a strong competitive edge and keen on long term growth and value.

Additionally, with a strong cash flow position (KES 88.5Bn), SCOM shows stout affiliation with its shareholders by offering to return excess capital by way of special dividends, KES 0.62 in FY19 (KES 0.68 in FY16).

Potential regulatory interventions are still possible despite the pending merger of Airtel and Telkom (32.4% market share).

These could be on certain product areas such as mobile money interoperability, new tariff approvals, fees on mobile loans, loyalty schemes and promotions. These potential regulatory controls could erode Safaricom’s competitive edge in these product segments.

(Last paragraph comment from Genghis Capital on the financial results)