Britam, Jubilee Insurance, Liberty Kenya and Kenya Re-Insurance are the best stocks to invest in Kenya’s insurance sector according to analysts at Genghis Capital.

However, they recommend a hold on CIC Group.

“CIC depicts potential for growth due to improving underwriting profits as the company focuses on claims management. Britam, on the other hand, will benefit from its wide regional expansion, cost containment and sturdy premium from the life business,” said the analysts in their Kenya Insurance Sector report themed ‘Out of the Woods’.

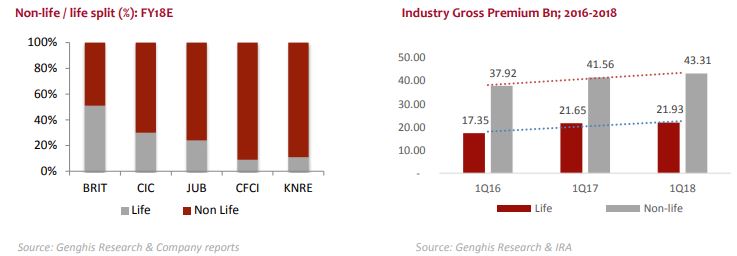

They project premiums to grow at an average of 8.7 percent in 2018 with non-life business expected to grow at a faster rate than the life insurance driven by an accelerating growth of 8.8% y/y in the non-life insurance business segment compared to a growth of 7.8% in the life business segment.

*****

CIC: We revise our SELL recommendation to a HOLD and raise our target price to KES 3.8 (from KES 3.13). This is on stronger premium improvement and an optimistic outlook on loss ratio reduction. We increase our TP by 16.7% to KES 3.8, pricing the stock at a P/E FY18E of 15x and P/B18E of 1.4x, against an industry median of 7.5x and 1.2x, respectively.

Jubilee: We update our recommendation on Jubilee with a BUY based on a fair value of KES 569.9. Our investment thesis is supported by; i) a solid 11.3% y/y growth in gross premium and a lower combined ratio forecast of 116.6% in FY18E against industry average of 105%.

Liberty: We update our recommendation on Liberty with a BUY based on a fair value of KES 16.4 against its market price of KES 12.6. This will be supported by i) a solid 5.95% y/y gross earned premium, ii) an 8% y/y investment income growth in FY18E. However, combined ratio remains a key concern. The stock remains cheap on a P/B of 0.9x against industry median of 1.2x.

Britam: We revise our rating from a HOLD recommendation to a BUY recommendation. We maintain our target price of KES 13.13 against current market price of KES 11.1. This is premium improvement (FY18E: 7.5% y/y) and an optimistic outlook on expense ratio improvement. High

claims ratio (FY18E: 68.8%) remains a concern.

Kenya Re: We reiterate our recommendation on Kenya Re with a BUY based on a fair value of KES 21.60. Our investment thesis is supported by; i) a solid 8.9 y/y growth in net earned premium, ii) a lower combined ratio forecast of 97.5% against industry average of 105% and iii) the stock remains cheap on a P/B of 0.5x against peer (Re-insurers) industry median of 0.9x.