The Central Bank of Kenya (CBK) continues to reiterate that interest rate caps have undermined the conduct of the monetary policy Committee.

In its draft report, ‘The Impact of Interest Rate Capping on the Kenyan Economy’ that calls for public comments states that using bank-level data covering the period before and after the interest rate capping law, coupled with selected macroeconomic indicators, our analysis shows that interest rate caps have started to yield negative effects which include the following:

First and foremost, the capping of interest rates has infringed on the independence of the central bank and complicated the conduct of monetary policy. It is found that under the interest rate capping environment, monetary policy produces perverse outcomes.

Secondly, there is evidence of reduced financial intermediation by commercial banks, as exemplified by the significant increase in the average loan size arising from declining loans accounts, mainly driven by the large banks, thus shunning the smaller borrowers.

Thirdly, banks have shifted lending to Government and the large corporates. Whereas demand for credit immediately increased following the capping of lending rates, credit to the private sector has continued to decline.

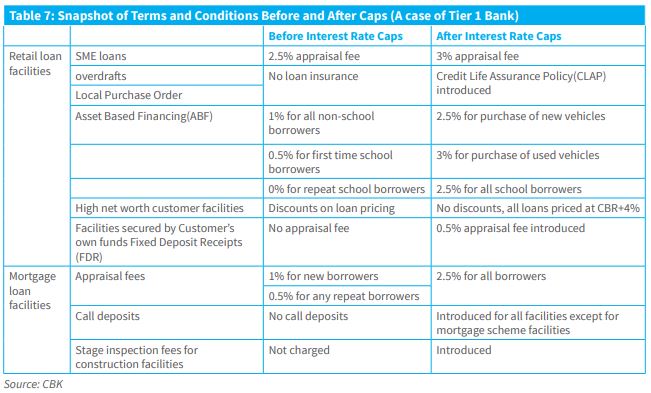

Fourthly, while the structure of revenue of the banks has started to shift away from interest income, some banks have exploited the existing approval limits to increase fees on loans in a bid to offset loss in interest income.

Fifth, although the banking sector remains resilient, small banks have experienced significant decline in profitability in recent months, which may complicate their viability.

Sixth, rationing out Micro, Small and Medium Enterprises (MSMEs) from the credit market by the commercial banks is estimated to have lowered growth in 2017 by 0.4 percentage points.

The Banking (Amendment) Law (2016) came into effect with the President’s assent on August 24th, 2016.

Read: What of the fiscal side as CBK reduce base interest

In January 2018 Dr.Patrick Njoroge, Governor CBK said “The interest rate caps have been acting as a brake to the economy. I don’t know if any of you have ever driven around with your brake still on. Eventually, something breaks.”

“The economy is being held back by this. And that is another set of issues we will bring to the fore and deal with so as to support, rather than inhibit economic dynamism in the economy,” he added post the Monetary Policy Committee meeting that left the policy rate unchanged at 10.00 per cent in its first meeting of the year maintaining its 17-month neutral policy stance.

In September 2016, the CBK Governor noted that Kenya’s decision to introduce caps was complicating monetary policy.

“Existing borrowers will benefit, but what happens to the risker borrowers at the margin? They may be cut off from lending. It’s unclear which way this will go. We haven’t done it before,” Njoroge had told reporters.

The limits on borrowing rates may result in a “perverse reaction” among banks and lead to riskier borrowers being cut off from lending, he said.

|

| Snapshot of Terms and Conditions Before and After Caps ( A Case of Tier 1 Bank) |

On the other hand, Cytonn Investments in 2017 stated that “The Banking (Amendment) Act 2015 has done more bad than good on the economy thus far, and if the situation is not arrested, could impact negatively on the economy.”

Besides Kenya being ranked as the fifteenth most attractive economy for investments flowing into the African continent, according to the latest Africa Investment Index 2016 by Quantum Global independent research arm, Quantum Global Research Lab, Prof Mthuli Ncube, Head of Quantum Global Research Lab states, “Supported by a stable macroeconomic environment, Kenya presents investors with relatively high exchange rate risk, low levels of liquidity and very low import cover.”

“However, going forward, the government policy of capping domestic interest rates is limiting growth on domestic credit to the private sector. This has the potential of being a drag on future economic growth, in an otherwise dynamic economy,” He adds.

Financial Times reported that the challenge, however, is with monetary and financial policy. Companies across the economy are suffering from the repercussions of a government-imposed cap on commercial interest rates.

On the other hand, the Central Bank Governor Dr. Patrick Njoroge says the banking sector has stabilized and strengthened underpinned by three pillars: enhanced transparency, stronger corporate governance and better business models.

And on the interest cap, in the African Business, April Issue he states that “We can’t say for sure how the interest cap will affect the banking sector, there is insufficient data available to us at the moment. What we can say for sure is that the average interest rates for the country have fallen.”

He adds that “Of course the cap will have an impact on profits, but they can still thrive without charging extortionately high-interest rates. We expect the cap will weaken bank’s balance sheets to a limited extent, but not dramatically.”

According to International Monetary Fund (IMF) mid-2017, sustained capping of commercial banks’ lending rates at 4 percentage points above the Central Bank of Kenya benchmark rate ‘if maintained, they could potentially pose a risk to financial stability,’ has warned.

“It is essential to remove these controls while taking steps to prevent predatory lending and increase competition and transparency of the banking sector.”

In the draft report, the CBK states “Going forward, under the interest rate capping regime, there is no guarantee the central bank will be able to achieve its intended objectives.”